There are so many things to consider when purchasing a commercial property. In my blogs I highlight dozens of important questions to resolve, I talk a lot about tenants, lawyers, bankers and agents, but one silent assassin for shooting down a property is whether it is subject to flooding.

As you know one of my favourite locations for securing shops at an attractive return is in Queensland. You will have heard the slogan about Queensland – “Beautiful one day, Perfect the next”.

However, many of us also witnessed with shock the January 2011 floods and saw the TV images of cities and towns near a river or watercourse go under water. In fact, the damage on the economy was so devastating the Federal government imposed a Queensland Flood Tax to help get the state back on its feet. So now when I’m buying a property in Queensland, a critical question I ask the agent is “Did the property get Wet Feet in the January 2011 floods?

If a property is prone to flooding or is listed in the council flood zone, then my advice in Engines of Wealth is simple – move on. I’ve sometimes heard agents say “Oh, it did but that was a one in 100-year flood”. The problem however is that it happened twice in 5 years in the case of Queensland. The impact of a flood can be catastrophic, not just the damage caused on the property but on the very survival of your tenant’s business. You see even if the damage on your property was minimal, the mud and debris left by these floods inside and outside the property takes weeks to clean up and at great cost. If the shop gets wet feet the water damage to internal gyprock walls, carpet and electricals results in thousands of dollars and many weeks of repair.

For many tenants, the water damage is not the biggest problem, it is the loss of trade while repairs are carried out and the time for consumer confidence to return that sends them into bankruptcy. As a buyer you need to understand the motivations of the Real Estate agent for a property that is prone to flooding. When asked by prospective buyers if the property floods, to say “Yes it does” means the buyer will run, to say “No it doesn’t” means a potential reporting breach.

Given their job is to sell the property they will quickly move you off the topic, over the years I’ve heard some great responses:

- “Great question, I don’t think so but let me check with the owner and come back to you”.

- Their hope is you’ll forget to raise the question again and fall in love with the property

- “It did back in 2011 but you must understand that was a once in a life time event”

- “It did get a little bit of water in it but hey it’s the tenants job to clean it up anyway”. Which is not entirely true: electricals, plumbing, roofing, wall integrity is the landlord’s responsibility.

- “Does it flood? Not to my knowledge.” If an agent did not ask and was never told by the current owners, that the property floods then an agent cannot be accused of telling a lie

- “It did but the council has done a lot of work to the drains since 2011 to prevent flooding.”

I have even had agents tell me that a property “to the best of their knowledge” hasn’t flooded only to have the tenant tell me it does and the next time it floods they’re not renewing their lease. As mentioned, for many tenants a flood can be a business ending event.

On the question of flooding, you must do your own research on the property and never rely on an agent’s comments.

There are some great websites that make your job a lot easier. If you’re buying a property in under the jurisdiction of the Brisbane City Council, your first point of research is “Floodwise”, see the link: https://www.brisbane.qld.gov.au/planning-building/planning-guidelines-tools/online-tools/floodwise-property-reports

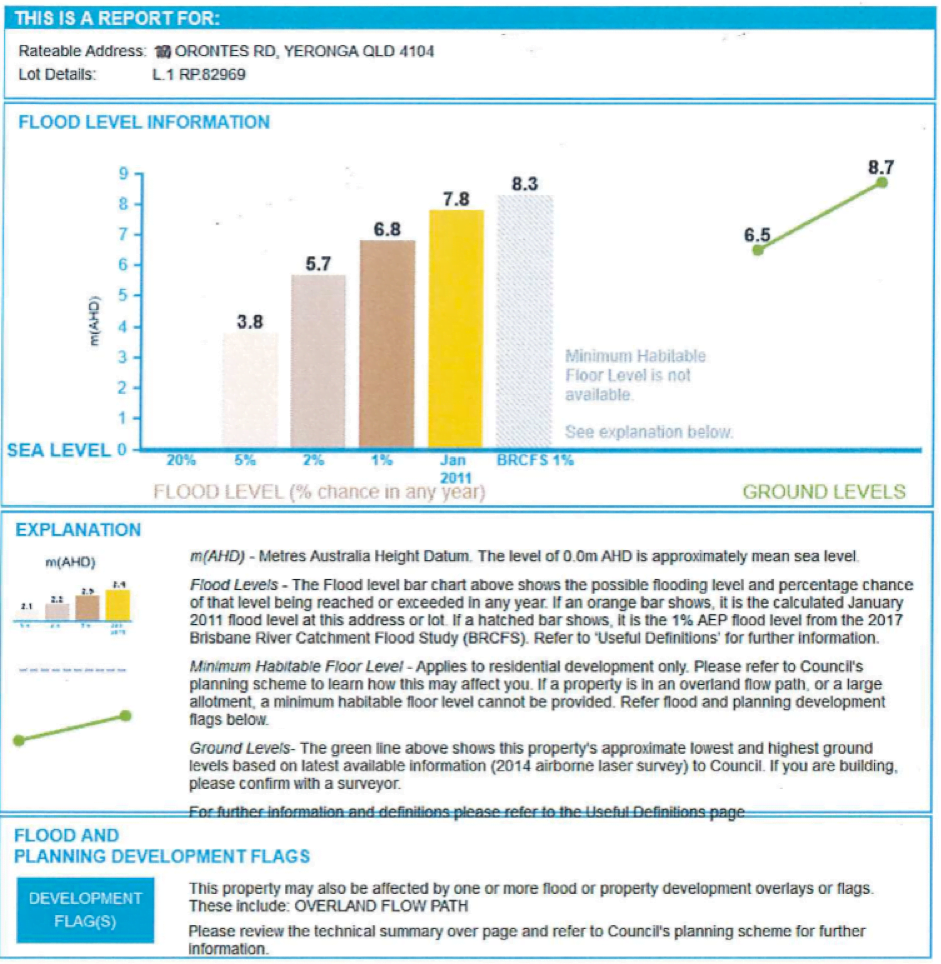

At this site you enter a specific property address and it will highlight if the property is in a flood zone and, it will tell you the minimum and maximum heights above sea level for that specific property. As an example, I was recently looking at a property in Orontes Road, Yeronga, Queensland and was concerned about possible flooding given the properties proximity to the Brisbane River. Typing in the specific address to the Floodwise website in seconds it returned the following report:

This graph shows the shop’s land at its lowest point is 6.5 meters above sea level and 8.7 meters above sea level at the highest point on the block. The chart as a reference also shows the level the water reached during the 2011.

Queensland floods at 7.8 meters. Therefore, some parts of the property were quite possibly underwater in 2011. Although this is not conclusive, this report raises alarm bells that require us to keep digging. The next research website I look to judge a property’s propensity to flood, is the council’s online flood maps. A great website is below, select the Flood Maps.

http://floodinformation.brisbane.qld.gov.au/fio/

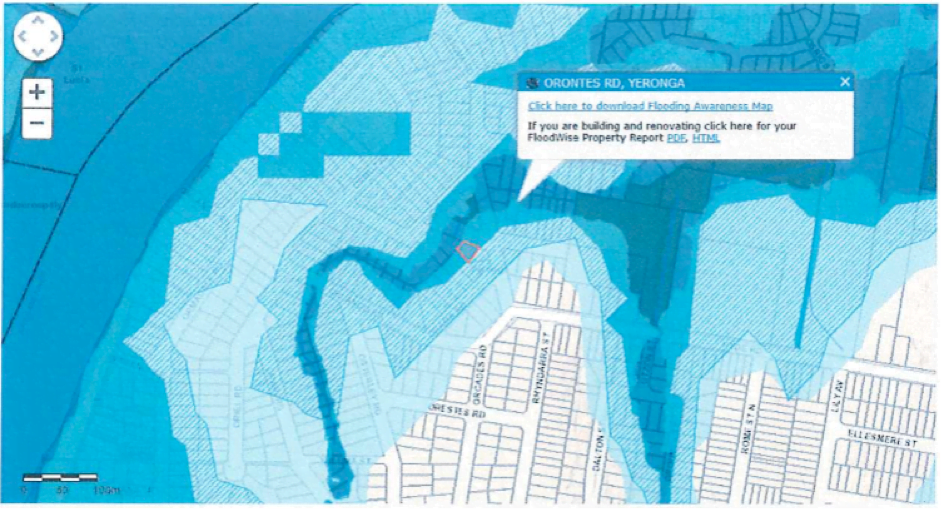

Once again, typing in the property address Orontes Road, Yeronga produces the following output:

The dark blue represents the areas that are most susceptible to flooding and the light blue represents the 1 in 100 year area. Cleary we can see the target property lies firmly within a flood zone and on the edge of the dark blue, this shop has a strong chance of getting wet feet during flood events.

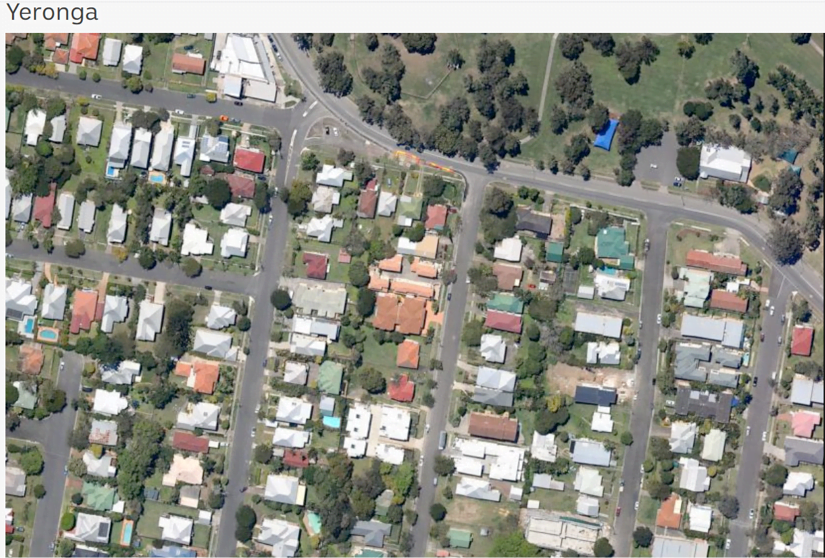

This evidence was enough to halt my interest in this property, however, if the shop had been on the flood fringe, then there is a third website I recommend you investigate. This site shows actual aerial photographs taken during the January 2011 Queensland floods.

https://www.abc.net.au/news/specials/qld-floods/

The website shows an aerial view of Yeronga before the floods:

Using a sliding TAB you drag across to see the aerial photo during the flood:

This site conclusively answers the question “Did the property it get wet feet in the 2011 floods?” I find these pictures really drive home the importance of doing your due diligence around flooding. It would be heart breaking to find the property you own under water.