When I speak with new clients starting their investment journey in commercial property, the first thing I need to understand is how financially ready they are to invest.

Understanding their available equity and how best to leverage it with the banks is critical. One practice that I see all too often is the diversification of lending across multiple institutions. Many investors believe there is safety in using different banks across their investment portfolio. This article answers the question: Does an investor benefit when they Diversify their loans or Should they Consolidate their loans with a single bank?

It is important to assess the pros and cons of using multiple lenders when building a portfolio of investment properties, as shown below:

| Diversify (Multiple Lenders) | Consolidate |

|

|

|

|

|

|

|

The four Diversify points above all sound like reasonable statements, however it would be extremely rare for a major lending institution to change their national lending policies to win your business especially if the loan being considered is less than $1,000,000. Therefore, whilst these motherhood thoughts of safety are comforting, I doubt in the heat of negotiations they would result in the outcome you anticipate.

In the book Engines of Wealth, we outline the top priority to build wealth is Leverage! In order to grow your investment portfolio, you need access to all of your equity, without this your ability to borrow will be restricted.

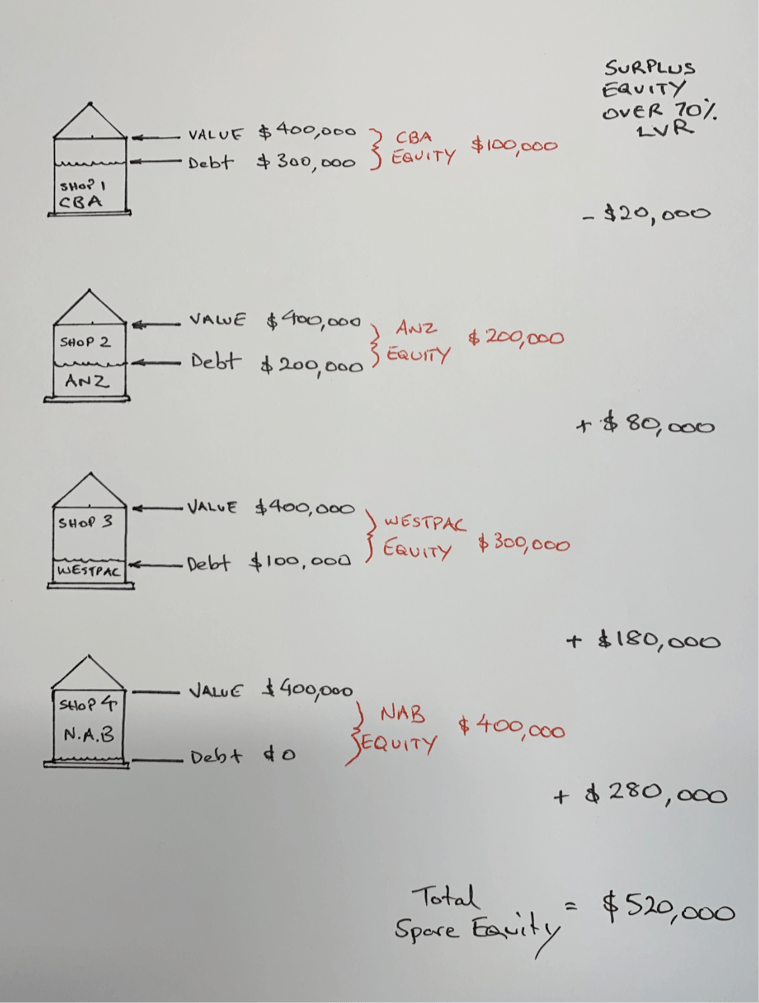

As an example, let’s take a look at an investor with a portfolio of 4 retail properties each with a purchase price of $400,000 and each with different residual amounts on the loans with four different banks. Then we will compare their borrowing capacity versus consolidating these four loans.

Example: 4 investment properties with CBA, ANZ Bank, Westpac and NAB

This investor has plenty of equity at their disposal. Each of the 4 properties are valued at $400,000 and the banks lend based on a typical 70/30 LVR (Loan to Value Ratio) position, then they would need to invest ($400,000 x 30%) = $120,000 of equity in each property. As shown in the above diagram, this investor has paid down the loans over time and currently has a total of $520,000 of available equity. The problem with this Diversified investment strategy is trapped equity! In total $280,000 of equity is stuck in NAB, $180,000 is trapped in Westpac, $80,000 is locked up with ANZ Bank and finally CBA may be charging this investor mortgage insurance because this LVR position is only 75/25, which is less than their standard 70/30 lending policy.

By diversifying these loans this investor is unable to cross collateralise their equity across the banks. They can only access the $520,000 in available equity to buy another property if they Consolidate the loans with one bank.

In addition to this, under the diversified model each bank would mandate rental payments be directed into the individual loans to meet their banks mortgage repayments while the more sensible approach for the investor would be to direct payments off a domicile loan that isn’t tax deductable.

Applying this example to a Consolidation strategy with all 4 loans with one bank, then this bank will hold security over all 4 shops. The total equity position is:

This is a very healthy LVR position. At 70% LVR the bank would lend $1,120,00 for this portfolio, hence with only $600,000 in remaining debt it releases $520,000 in spare equity to procure an additional property.

Based on the same 70/30 LVR, this investor would be able to buy a 5th property valued at:

Using a Diversified strategy to buy a 5th property, this investor could at best leverage the $280,000 equity available with NAB to buy a property valued at:

Diversifying your loans traps equity within individual banks and makes it very hard to leverage all of your available equity.

The team at Engines of Wealth would be happy to assess your situation and provide our experience on unlocking your full borrowing potential.

________________

Please contact the Engines of Wealth team if you have any questions:

stephen@enginesofwealth.com

phillip@enginesofwealth.com