When I first spoke with Phillip to understand his commercial property investment secrets, I quickly realised this was an investment strategy and asset class suited to my personal financial strategy. I undertook a one-on-one consulting session with Phillip for over 3 hours and was inspired by the possibility of creating a long-term income stream. I immediately began scouring the websites for attractive retail shops. I now own 12 retail shops that are fully tenanted and serve as the foundation for my current and future income plans.

With this background, let me step back in time to the very first question I asked when I decided commercial properties were going to be my future income engine:

“How many shops will I need to ensure I have enough income to last until I die?”

Whether you are a savvy 22 year-old with a small deposit or 50 years old looking to leverage assets you’ve accumulated over 30 years of work, setting a future plan to have sufficient cash for comfortable retirement living is important. Many people today just survive on their retirement income and pension, they don’t have enough money to really live. I was in my late 40s when I spoke with Phil. At that time, I had just paid off my home, I had stopped working for a large corporation and went into business for myself.

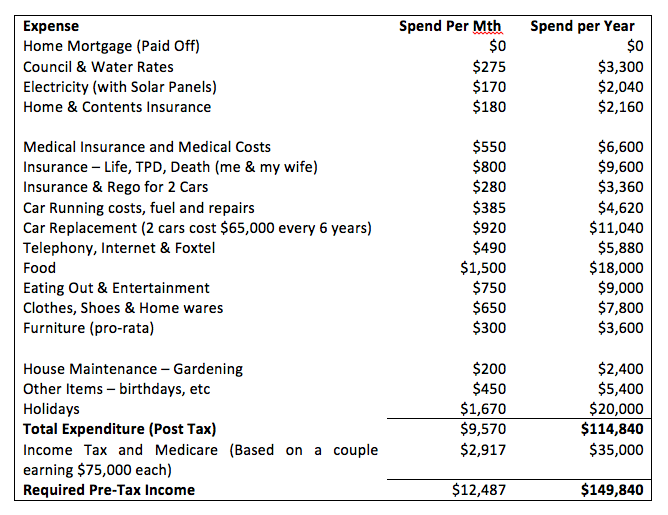

For me it was a great time to think about life after work, or at least a simpler life working part time, and the question I needed to understand was how much money do I spend in an average year/month. I captured my expenditure in the table below as a starting point. Of course, this amount will vary from one individual to another depending on aspirations, but it is useful as a reference point for my target shop rent. The two assumptions I have made is that my house was paid off and the kids are no longer at school or university.

My post tax monthly expenditure was $9,570 per month or just under $115,000 a year. Therefore, as a starting point my wife and I need to split almost $150,00 pre-tax income to live our existing lifestyle.

In setting a long-term income target for my retirement, I reflected that today’s costs will be indexed to inflation and that cost increase will be covered by the income generated from the shop rents that are also indexed to inflation by annual rent increases. So these net out making my calculation on the money I’d require in the future easier. I decided that the $150,000 I need today is a comfortable annual income target to adequately fuel my retirement. Others may require more or less, but this amount sets my income bar to answer the question of how many shops I need to retire.

At present, the income generated from my 12 retail shops is combined with income generated from my business to sustain my family. Over the next 10 years, I plan to pay down my investment loans and acquire more retail shops until the annual income from the shops alone reaches my retirement target of $150,000 per year. Defining when I have enough shops in my portfolio to fuel my retirement, comes down to a simple formula:

Cumulative Shop Net Rent – Bank Interest for the Shop Loans ≥ $150,000 per year

At present, my portfolio of 12 shops is secured by my home as security. It is important to continue leveraging the equity from my house and these existing shops to procure more shops. At present, my shops generate $181,000 in net rent. The loans on the shops total $2.35m resulting in an annual interest bill of $108,000 per year. Plugging these figures into the ‘retirement’ equation shows:

$181,000 – $108,000 = $73,000

By this calculation I am almost halfway ($73,000) towards my $150,000 target from the 12 shops I have today.

To achieve my retirement income target I will need shops generating almost $360,000 in net rent annually (double the $181,000 I have today). Now to collect this amount of net rent there are positive and negative forces that will speed up my shop income journey or slow it down, some of these are:

Positive Forces

- Annual rent increases built into the lease will keep my cash flows indexed better than inflation

- Market rent reviews on lease expiry may lift rental returns faster than CPI

- Income from my job and the shops will continue to pay my loans down reducing my interest bill and increasing my annual cash flows

- The reserve bank may lower interest rates over the next 10 years

- Population growth in the selected areas I choose to invest may drive rents up with increased demand

- By structuring my investments optimally to manage the tax burden, placing some shops in my wife’s name

- The government may lower personal tax rates.

Negative Forces

- A tenant vacancy over the period will compromise the income in that year

- The Reserve Bank may increase interest rates over the next 10 years

- A softening economy may place downward pressure on rents

- The government may abolish deductions available to commercial property owners, for example, travel expenses to visit the commercial property, negative gearing from temporary vacancy

- The government may increase my tax rate.

All of these ups and downs are possible, but I am confident that once I achieve my target of $150,000 in annual shop income, it is sufficient and indexed with inflation to grow in-line with the cost of living. In essence, I believe the annual increases and market reviews built into the shops’ leases are future-proofing the net rent and my retirement income. Furthermore, I am confident that in following Phil’s directions, as outlined in Engines of Wealth, I have selected properties that are secure and strong in tenancy to optimise these ups and downs.

Armed with this insight the question “How Many Shops do I Need to Retire?” should be redefined to “How many shops do I need to generate my target retirement income of $150,000?”. Presuming I need to collect 24 shops (double my 12 today) to retire is a false target, this implies all shops are the same, some shops are big and some shops are small, some generate $40,000 in gross rent and others can generate over $400,000. Keeping it simple, I borrowed $2.35m to secure half my target income from shops that on average deliver a 7.5% return on my investment. Assuming I secure future shops at this return and continue to borrow 100% of the property amount, I will need a property portfolio supporting borrowings of $4.7m, that’s roughly double the debt I have today.

Among all of these numbers, the key figure to focus on is the retirement income target, for this will dictate the number of shops needed. As I am halfway into my commercial property investment journey, I agree with something Phillip says in the book, “there is always room for one more”. Happy hunting.

Written by Stephen Hains